WHAT IS IT?

Credit score is a number scale between 300-850 that reflects your credit worthiness. This number is based on credit history: number of open accounts, credit utilization, and repayment history among other factors. Lenders use credit scores to evaluate the financial stability of a consumer, particularly the probability that loans will be paid in a timely manner. The higher the score, the more reliable the consumer looks to potential lenders. Credit score is important; having good credit will make it easier to borrow money, reduced premiums, lower interest rates on loans and credit cards, and make it easier to rent an apartment or buy a home.

TYPES OF CREDIT SCORES?

There are three major credit bureaus: Equifax, Experian and TransUnion. They don’t share information with each other, meaning your credit score can be different for all three. For example, if you had an excellent credit score for one bureau, it might be considered good for the other two. Credit scores are divided into 2 main scoring models: FICO and VantageScore.

FICO Model

FICO, otherwise known as Fair Isaac Corporation, was developed in 1989. According to MyFICO, over 90 percent of top lenders use FICO credit scores when making lending decisions.

FICO Credit Score Ranges:

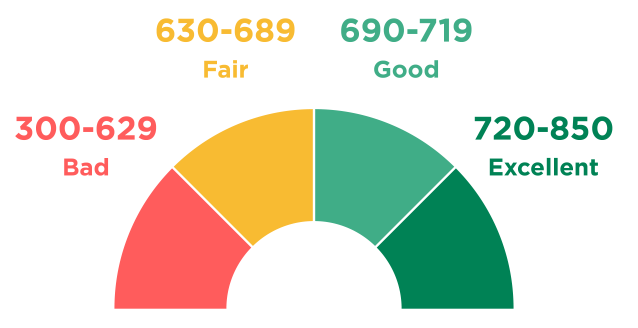

EXCELLENT: 800 TO 850 VERY GOOD: 740 TO 799 GOOD: 670 TO 739 FAIR: 580 TO 669 POOR: 300 TO 579

VantageScore Model

The three major credit bureaus, Equifax, Experian and TransUnion created the VantageScore model in 2006 as an alternative to the FICO scoring model.

VantageScore Credit Score Ranges:

EXCELLENT: 781 TO 850 VERY GOOD: 661 TO 780 GOOD: 601 TO 660 FAIR: 500 TO 600 POOR: 300 TO 499

Other Credit Score Models

Other than FICO and VantageScore, there are other models. Equifax created its own scoring model, but the scale goes from 280-850. Other credit score providers offer their own score models, but it’s just based on the FICO or VantageScore models.

HOW DOES IT WORK?

Your credit score affects your financial life, it plays a considerable role in a lender’s decision to extend your credit. Based on FICO credit scores, individuals with a credit score of 640 or lower are considered “Subprime Borrowers”. This means that a person is identified as a high risk borrower for a lender.

What exactly makes an individual a subprime borrower? When lenders are analyzing a subprime borrower’s credit history, they are most likely to have multiple negative factors, such as delinquencies and rejections. It can also mean that the borrower has a short credit history, meaning that they either have little or no credit reports at all.

Lending companies would consider giving a loan to the individual borrower, but it would be a “Subprime Mortgage”.

A Subprime Mortgage is a type of mortgage that’s only provided to Subprime Borrowers. This type of loan has a higher interest rate as the borrower is considered a greater risk.

A borrower’s credit score also determines the size of an initial deposit to obtain services and an apartment.

Factors that affect your credit score:

- New Credit: This tracks how many “hard inquiries” you have when you apply for new credit. It can nick your score for up to six months.

- Length of Credit History: This refers to how long you’ve had credit and the average age of your credit accounts.

- Credit Mix: Having both installment loans (those with level payments, like a car loan or mortgage) and revolving credit (like a credit card) can help your score.

- Amounts Owed (Credit Utilization): This is how much of your available credit you are using — the less it is, the better for your score.

- Payment History: Late payments can really hurt your score, as can accounts in collections or a bankruptcy.

Chart from What Is a FICO Score?

Chart from What Is a FICO Score?

How to Improve Your Credit Score

- Pay your bills on time: Six months of on-time payments is required to see a noticeable difference in your score. Missing one payment will hurt your credit score.

- Up your credit line: If you have credit card accounts, call and inquire about a credit increase. If your account is in good standing, you should be granted an increase in your credit limit. It’s important not to spend this amount so that you maintain a lower credit utilization rate.

- Keep credit balances low: This helps lenders know how well you can manage credit. Using too much is a warning sign for lenders.

- Don’t close a credit card account: If you are not using a certain credit card, instead of closing it, just leave it to the side. Depending on the age and credit limit of a card, closing the card may be detrimental to your credit.

HOW CAN I MONITOR MY CREDIT?

You can monitor your credit on a daily basis, using various apps and websites. You can help protect your credit by freezing your credit. It’s the best way to prevent any new account from being opened in your name. You can do it as many times as you like, and it won’t affect your credit score.

You can also see your full credit report from each bureau for free once a year. Use it wisely, before a major purchase, such as a car or a home. You can visit annualcreditreport.com to see your full credit report.

Contact us for additional information about credit reporting and steps on how to improve it.